Contents

The Enhanced R&D Intensive Support (ERIS) scheme is a specialist form of R&D Tax Relief introduced in April 2024. It’s designed for loss-making SMEs that invest heavily in innovation, offering a higher level of support than the standard merged R&D scheme.

As part of the 2024 reforms, ERIS replaced the enhanced element of the SME scheme for R&D-intensive, loss-making companies, while most businesses now claim under the merged scheme.

To qualify, companies must spend at least 30% of their total expenditure on R&D. For those that do, ERIS can provide a significantly increased cash benefit, helping to support ongoing development and growth.

While this guide explains how the ERIS scheme works, we recommend speaking to an R&D tax specialist to ensure your claim is accurate and fully optimised.

What is the ERIS scheme?

Enhanced R&D Intensive Support (ERIS) forms part of the UK’s wider R&D Tax Relief system, providing enhanced support for a specific group of businesses.

It focuses on loss-making SMEs with a high level of R&D investment, typically where a significant proportion of overall costs are tied to innovation.

Under ERIS, companies can benefit from:

- An 86% enhanced deduction on qualifying R&D expenditure

- A 14.5% payable tax credit on surrendered losses

- An overall benefit of up to around 27% of eligible R&D spend

Why was the ERIS scheme introduced?

ERIS was introduced as part of the UK’s R&D Tax Relief reforms to ensure that businesses investing heavily in innovation continue to receive meaningful support.

Under the previous SME scheme, loss-making companies carrying out significant R&D could access higher levels of relief. As the system moved to a merged scheme, ERIS was introduced to preserve that level of support for companies that are both loss-making and R&D-intensive.

In practice, ERIS helps ensure that early-stage and innovation-led businesses maintain cash flow and continue investing in development, even before reaching profitability.

Who qualifies for the ERIS scheme?

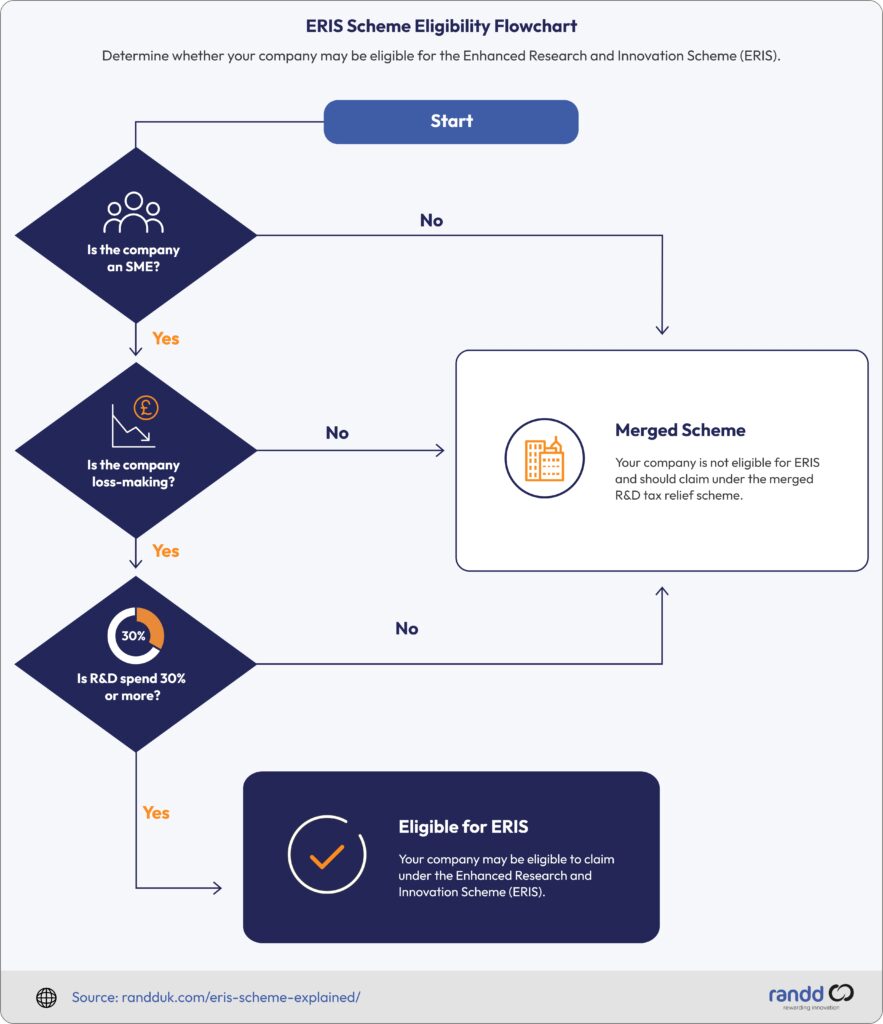

To qualify for the Enhanced R&D Intensive Support (ERIS) scheme, companies must meet specific criteria relating to their size, financial position, and level of R&D investment. The infographic below highlights the three key requirements businesses must satisfy to be eligible for ERIS tax relief.

1. SME status

Your company must meet the UK definition of a small or medium-sized enterprise (SME). This generally means:

- Fewer than 500 employees

- Turnover under €100m

- Or a balance sheet total under €86m

These thresholds may also take into account linked or partner enterprises where relevant.

2. Loss-making companies

ERIS is only available to SME companies that are loss-making for tax purposes.

Rather than carrying losses forward, eligible businesses can choose to surrender those losses in exchange for a payable tax credit, providing a valuable source of funding while continuing to invest in research and development.

3. R&D intensity threshold

To qualify, loss-making SME companies must spend at least 30% of their total expenditure on qualifying R&D activity.

This threshold was reduced from 40% to 30% as part of the April 2024 reforms, making the scheme accessible to a wider range of R&D-intensive businesses. Eligibility is assessed for each accounting period, meaning it can change over time.

Companies must therefore meet the SME definition, be loss-making for tax purposes, and spend at least 30% of their total expenditure on qualifying R&D to access ERIS. If you want a deeper breakdown, see our guide on who can apply for the ERIS scheme.

R&D intensity calculation for the ERIS scheme

R&D intensity is the key measure used by HMRC to determine whether a company qualifies for ERIS.

It compares how much of your total business expenditure is spent on qualifying R&D. To be eligible, at least 30% of your overall costs must relate to R&D activity.

The calculation is based on:

- Qualifying R&D expenditure (the numerator)

- Total company expenditure (the denominator)

Total expenditure includes all costs in your profit and loss account, not just R&D spend. In broad terms, this means the costs that contribute to profit before tax.

If your company is part of a group, you’ll need to include expenditure from connected companies when calculating R&D intensity. This applies where companies are linked or under common control, meaning HMRC requires the calculation to reflect total expenditure across the wider group.

This can include overseas companies or those with different accounting periods, where costs may need to be split between periods. You can find more detail in HMRC’s official guidance on the ERIS scheme.

ERIS R&D intensity formula

R&D intensity = Qualifying R&D expenditure ÷ Total company expenditure.

To qualify for ERIS, your overall result must be 30% or higher, as shown in our example below.

Example R&D intensity calculation

Total company expenditure:

| Expense | Amount |

| Staff costs | £375k |

| Rent | £95k |

| Software | £60k |

| Total expenditure | £530k |

Qualifying R&D expenditure (included within the above): £240k

R&D intensity = £240k ÷ £530k = 45%

In this example, the company exceeds the 30% threshold and would qualify under the R&D intensity requirements.

What counts towards total expenditure?

Total expenditure includes all costs recorded in your company’s accounts, such as:

- Rent and overheads

- Staff costs

- Subcontractor costs

- Software

- Operational expenses

Only qualifying R&D costs are included in the R&D portion of the calculation. This means that while all business costs contribute to the total, only eligible R&D spend is counted towards meeting the 30% intensity threshold.

How much tax relief can you receive under ERIS?

ERIS provides a higher level of support than the standard merged R&D scheme for companies that qualify.

Qualifying R&D expenditure receives an 86% enhanced deduction, increasing the total deductible amount to 186% of the original spend. For loss-making companies, this enhanced loss can then be surrendered in exchange for a payable tax credit.

The credit is paid at a rate of 14.5%, resulting in an effective benefit of up to around 27% of qualifying R&D expenditure, depending on the company’s tax position.

In practical terms, this means that for every £100 spent on eligible R&D, a company could receive up to £27 back as a cash payment.

The final amount received may also be affected by factors such as the PAYE cap, which can limit the payable credit based on a company’s payroll, as well as its wider tax position.

This additional support is intended to help innovation-led SME businesses maintain momentum, reinvest in development, and manage cash flow during their growth phases.

Example ERIS calculation

If a company spends £100k on qualifying R&D:

- Enhanced deduction:

£100k x 186% = £186k

- Payable credit (if losses are surrendered):

£186k x 14.5% = £26,970

This creates a cash credit of £26,970, equivalent to an effective benefit of just under 27%.

In practical terms, that’s almost £27 back for every £100 spent on R&D.

If you want to get a more accurate estimate based on your own figures, you can use our R&D Tax Credit calculator.

ERIS vs the R&D merged scheme

| ERIS | MERGED |

| Loss-making SMEs | Most companies |

| 30%+ R&D intensity | No intensity requirement |

| 27% benefit | 15-16% benefit |

Following the April 2024 reforms, most companies now claim R&D Tax Relief under the merged scheme, as ERIS is only available to businesses within a specific criteria.

Use the flowchart below to quickly determine whether your company may qualify for ERIS or should instead claim under the merged R&D scheme.

You can read more about this in our guide to what changes were made to the R&D Tax Credit schemes.

It applies to loss-making SMEs that meet the R&D intensity threshold, while the merged scheme covers the majority of companies, including profitable businesses and those with lower levels of R&D spend.

| Scheme | Who qualifies | Typical benefit |

| ERIS | Loss-making R&D intensive SMEs | Up to 27% |

| Merged scheme | Most companies | 15-16% |

Companies may move between schemes depending on their individual circumstances. For example, if R&D intensity falls below 30%, or the company becomes profitable, it will typically claim under the merged scheme instead.

Since eligibility can change between accounting periods, understanding which scheme applies and how to maximise your claim isn’t always straightforward. In these situations, working with an R&D tax specialist can help ensure you’re claiming under the right scheme and getting the full benefit available.

What R&D costs qualify under ERIS?

The costs that qualify as R&D expenditure under the ERIS scheme are broadly aligned with the wider UK R&D Tax Relief framework. These are the costs that can be included in your claim, rather than your total business expenditure.

Here’s a breakdown of those that typically qualify:

Staff costs

This includes salaries, employer National Insurance, and pension contributions for employees who are directly involved in R&D activities. Where staff split their time, a proportion of their costs can still be claimed.

See our guide on who counts as an employee when calculating R&D Tax Relief claims for more clarity.

Subcontractor costs

Payments to subcontractors carrying out R&D work on your behalf may be eligible, depending on the contractual arrangement and where the work is performed.

Consumables

Materials used up or transformed during the research and development process are deemed as ‘consumables’ and can be included in your claim. This typically covers items used in testing, prototyping, or development. You can read our guide to consumable items to get a better understanding.

Software

Software used directly in R&D activities can be included in your claim, and often includes development tools, modelling software, and testing environments.

Data

Data licences and cloud computing services used in R&D can be included, such as storage, processing power, and development infrastructure.

What happens if a company no longer qualifies for ERIS?

If your company no longer meets the ERIS scheme criteria, you can typically claim through the merged R&D scheme for that accounting period.

Reasons this may happen include:

- R&D intensity falls below the 30% threshold

- The company becomes profitable rather than loss-making

As the GOV.UK website specifies, you generally must meet the qualifying conditions for the period you’re claiming for.

In some cases, a one-year grace period may apply. This allows companies that previously qualified as R&D-intensive to continue claiming under ERIS for a limited period, even if their R&D spend temporarily falls below the threshold.

This helps provide continuity for businesses whose investment levels may fluctuate over time.

Can companies choose between ERIS and the merged scheme?

Companies may be eligible for ERIS and the merged scheme, but they can’t claim under both schemes for the same expenditure. In practice, ERIS is usually the more valuable route for loss-making, R&D-intensive SMEs, but eligibility should be assessed for each accounting period.

How to claim ERIS Tax Relief

ERIS claims are submitted as part of your company’s Corporation Tax Return (CT600).

To make a claim, companies must:

- Complete the additional information form outlining their R&D activities

- Provide a clear technical explanation of the work undertaken

- Include a detailed breakdown of qualifying costs

Claims must be submitted within two years of the end of the relevant accounting period.

Since a high level of detail is required, it’s important to ensure that both the technical and financial aspects of the claim are accurate and well documented. This can help reduce the risk of delays or enquiries from HMRC.

Some companies may also need to submit a claim notification before making their claim.

ERIS scheme FAQs

ERIS stands for Enhanced R&D Intensive Support, as it’s designed to provide a higher level of support to a particular group of businesses that meet its criteria.

The HMRC ERIS scheme is a form of R&D Tax Relief for loss-making SMEs that spend at least 30% of their total costs on R&D.

At least 30% of total expenditure must be spent on qualifying R&D.

R&D intensity for the ERIS scheme is calculated by dividing qualifying R&D expenditure by total company expenditure.

The ERIS Tax Credit rate is 14.5% on a company’s surrendered losses.

Up to approximately 27% of a company’s qualifying R&D spend.

No, ERIS is only available to loss-making SMEs.

The ERIS scheme started for accounting periods beginning on or after 1 April 2024.

ERIS replaces the enhanced support element for loss-making, R&D-intensive SMEs under the current system.

Adam Bointon is a Technical Director specialising in R&D Tax Credits for SMEs in manufacturing and software sectors. With over 15 years’ experience, he works closely with businesses to identify qualifying R&D activities and prepare clear, compliant claims. He combines technical expertise with a strong understanding of economics and finance to support successful outcomes. Adam also contributes to industry webinars and CPD sessions, sharing insights on R&D tax relief and HMRC requirements.

Sign up to our Newsletter

Stay ahead with the latest R&D tax insights, funding updates, and innovation trends — straight to your inbox.